I really do not like this deal.

The Stink of Life Insurance

In fact, I don't like anything that has a whiff of life insurance to it.

Life insurance and annuities are super long duration contracts and your P&L involves projecting out 20 years plus. That high level of of uncertainty means your financial statements are basically made up of layers and layers of assumptions (mortality/longevity, interest rates, equity index levels...etc).

This is why life insurance peers like Prudential (PRU), Metlife (MET), Lincoln (LNC) and so on all trade around 10x P/E. Don't let anyone tell you it's all about the low rates depressing investment income!

No, the very business model of life insurance and annuity is shit, period.

I would actually frown upon growth in this business, as growth would indicate the company is taking on more risk to bring in more business.

Now, I'll admit FGL's index annuities are less risky than the notorious variable annuities with guarantees. In those old GMDB/GMIB/GMDB products, policy holders invest in stock funds and the companies guarantee some minimum amount of return. These companies essentially sell a giant put option, exposing themselves to egregious losses during down markets. Index annuities, on the other hand, are newer derivative products (yes that's what it is). They are less risky because issuers essentially buy a bunch of call options on equity indices, and pass through the benefit to policy holders. Buying calls is less risky than selling puts!

A couple diagrams below show my understanding of how these products work. Notice that both the older GMxB and the new Index Annuities (FGL's products) give customers limited downside, but the latter incurs vastly better risk from insurer perspective.

So yes, FGL's annuities are much less risky than those notorious products of old. Still, over the life of a policy a lot of stuff can go wrong. FGL sells a derivative product with all sorts of market risks. I do not trust the financials.

Frankly, I doubt that FGL will ever shake off the stink of life insurance and the black box/ high risk stigma associated with it - even if rates go up. In other words, FGL will likely be a low multiple business forever. Even if it has high growth.

Is FNF Serious?

The first question is: is this actually a strategic acquisition, or it's just Bill Foley doing what he does - bring in some company only to spin it out later?

I told you above I hate the annuity business. So naturally, I hope it's the latter.

"Strategic acquisition" would be a big problem. As a shareholder, I don't want to see FNF deploy its abundant free cash flow toward growing a unrelated and shitty business that will never fetch a high multiple!

Unfortunately, the the 2/7/2020 conference call to discuss the acquisition seem to indicate otherwise. Management spoke of FGL as a strategic diversification and brought up examples of acquisition benefits, all of which are questionable.

As an example, they talk about FGL business smoothing out the combined company's exposure to interest rate changes. This is hogwash and they know it. FNF's refi business are already burned out from years of low rates and can't get hurt much more from higher rates. Also, it's not like FNF doesn't have its own investment operation that will benefit when rates go up!

Management also argued that FGL can benefit from FNF's bank relationship. In that very same call, FNF management actually backtracked from that assertion when challenged by analysts. The benefits will be limited to small time distributions.

I came away from the 2/7/2020 call feeling unsettled, but still hoping this is just Bill Foley playing the spin-off game.

Then came the 4Q19 earning call on 2/14/2020.

It Gets Worse!

In the 4Q19 call, FGL's CEO Chris Blunt tried to address some of my concerns above and tried to argue that FGL is not quite a life insurance business. I think he failed.

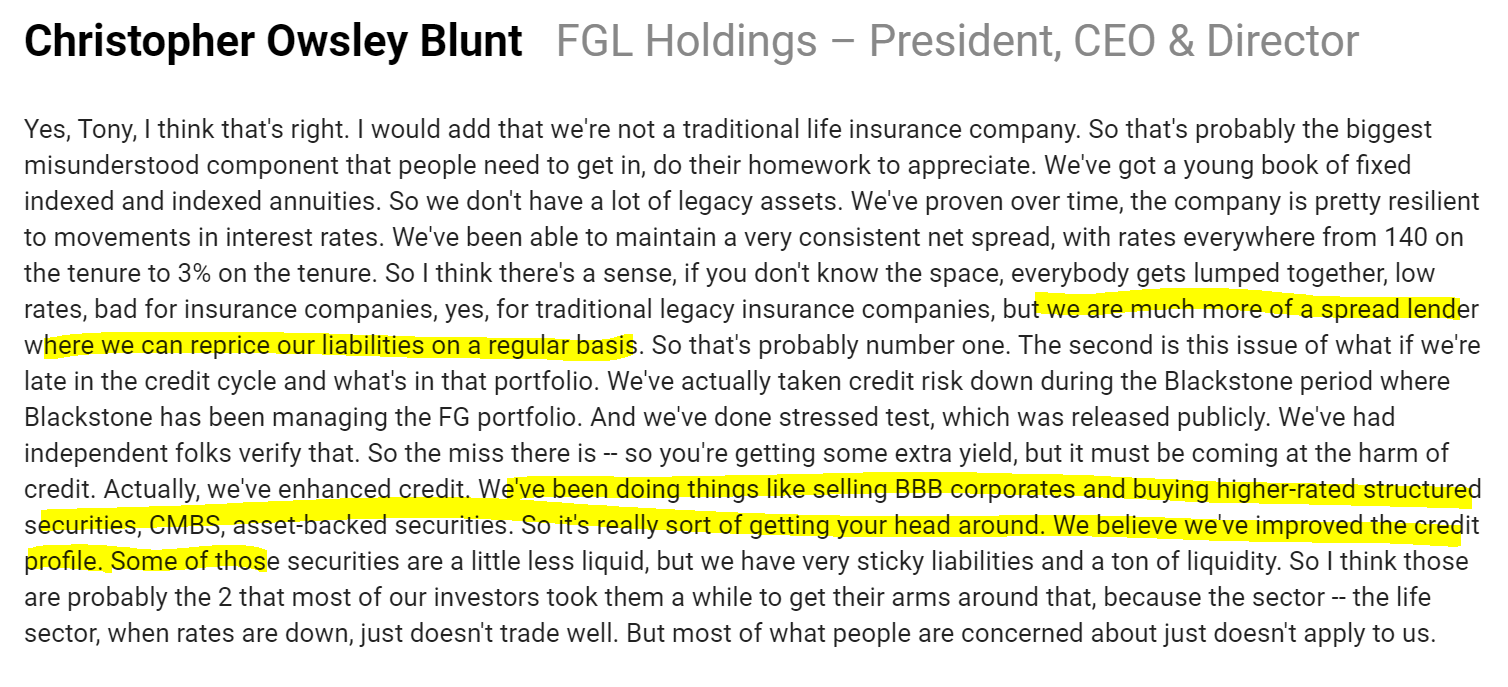

The first point:

"We are much more of a spread lender where we can reprice our liabilities on a regular basis".This is somewhat valid and very important. It corroborates my earlier point that index annuities are less risky than the older variable annuity products.

Repricing liabilities is important because that shortens the duration, making them less sensitive to key macroeconomic factors.

That lessens the pain but doesn't make it go away. I would rather the company NOT take on these liabilities at all! (per FGL's 10K for 2018, liability duration is ~6.2 years).

The second point about improving credit quality brings back nightmares. AAA rated CDO-squared anyone? After the 2008 debacle, how anyone can still equate credit rating with actual risk is beyond me.

- Talks about FGL doubling its AUM in 5 years with resource of FNF, could be 50% of FNF's overall earnings. (sounds awful!)

- Apparently FGL has ambition in pension risk transfer. (PRT = WTF!!!)

- Talks about giving Blackstone more money to manage.

- Talks about FGL increasing investment yield without compromising on risk - by switching from BBB corporates to higher rated ABS and CMBS.

Good Fucking God!

I even get the impression Bill Foley is looking at FGL's Chris Blunt as some sort of successor. The latter is not exactly young, But it's hard not to get that impression when Foley talk about FGL growing to 50% of overall company earnings, giving Chris Blunt more money to manage, and basically let Blunt talk nonsense like chasing yield with structured products and pension risk transfer.

Second, even if that's true, why would I trade a steady service business (which is what title insurance actually is) leading an oligopoly, with a "spread business" that has little entry barrier?

Conclusion

I suppose one can argue "of course Foley has to talk like it's a strategic acquisition, of course that's what he says now. Just wait a couple years and he'll spin it out, just watch".

Even if that's the case, FGL is not like FNF's past acquisitions. Black Knight, Ceridian...etc, these are growth companies that has a ready market when the time comes for exit. I don't see that for FGL - it's just not a high multiple business.

After several years of holding FNF (and as my largest position the past 2 years). I will have to exit or at least cut down drastically.

Thankfully it's a long weekend now. I will have time to sleep on it.

No comments:

Post a Comment